CSRD Reporting: Key things to know about CSRD and ESRS in 2024.

In 2019, the European Commission launched the European Green Deal, charting a course for Europe to become the world's first climate-neutral continent. Central to this mission is fostering a green economy, directing investments towards sustainable ventures.

Legislative acts like the EU Taxonomy and the Corporate Sustainability Reporting Directive (CSRD) are pivotal in advancing this agenda. The EU Taxonomy sets clear criteria for activities to qualify as "sustainable," empowering investors to align with green goals.

Meanwhile, the CSRD replaces the Non-Financial Reporting Directive (NFRD), ushering in comprehensive Environmental, Social, and Governance (ESG) reporting requirements. By standardizing reporting and enhancing transparency, the CSRD propels Europe towards a more sustainable future.

1. What is the CSRD and what are ESRS?

The CSRD, in effect since January 2023, mandates annual sustainability reporting for companies within the European Union. European Sustainability Reporting Standards (ESRS), endorsed in July 2023, delineate specific reporting requirements, facilitating comprehensive sustainability assessment.

The CSRD requires that companies transparently report their sustainability performance annually, replacing the prior Non-Financial Reporting Directive (NFRD). This extends coverage from 12,000 to 50,000 companies, including those outside the EU.

Additionally, the European Commission approved the European Sustainability Reporting Standards (ESRS) in July 2023. These standards specify reporting requirements for each topic, facilitating improved comparison and monitoring of sustainability performance across companies.

2. Who does the CSRD apply to?

Many companies face uncertainty regarding CSRD compliance timelines, risking reputational damage and sanctions for non-compliance. Here's a simplified timeline:

By 2025: Companies under NFRD regulations report on 2024 sustainability performance if meeting at least two of the following criteria:

> 500 employees

> 40 million Euros revenue

or > 20 million Euros total assets.

From January 2026: Large European companies report on 2025 sustainability performance if meeting at least two of the following criteria:

> 250 employees

> 40 million Euros revenue

or > 20 million Euros total assets.

From January 2027: Listed European SMEs report on 2026 sustainability performance if meeting at least two of the following criteria:

> 10 employees

> 700,000 Euros revenue

or > 350,000 Euros total assets.

From January 2029: Non-European companies with at least one subsidiary or branch in Europe and >150 million Euros turnover report for the first time, covering 2028.

3. What does it take to comply with CSRD?

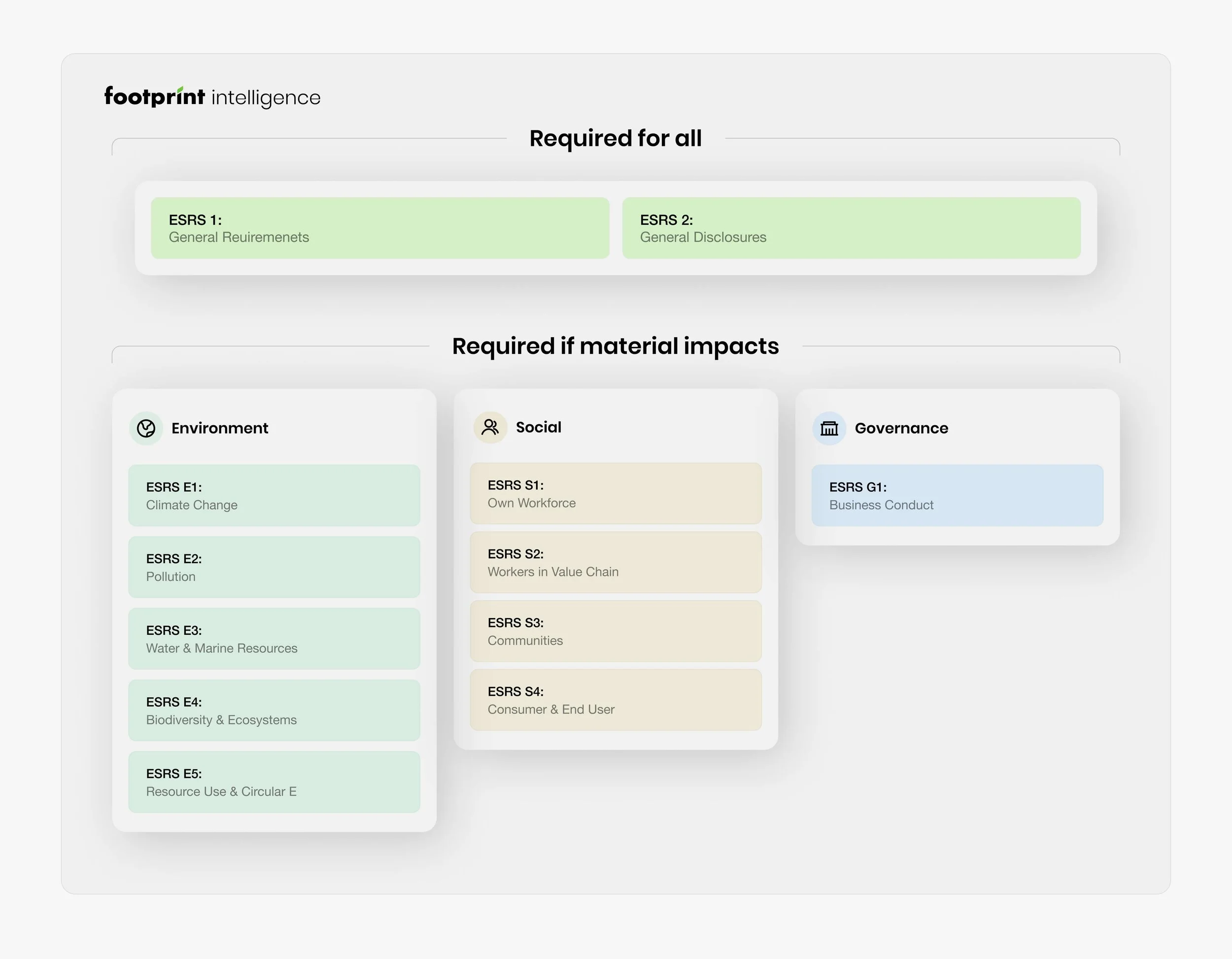

The CSRD relies on 12 European Sustainability Reporting Standards (ESRS) to define reporting criteria. These standards, applicable across all sectors, include two overarching standards applying universally, and 10 thematic standards covering various ESG topics. Companies report only on standards deemed material or relevant based on their materiality analysis.

To comply with CSRD, companies must disclose their sustainability strategy, impact, and targets, with reports verified by a neutral third-party auditor, akin to financial reporting requirements. Companies should refer to the European Sustainability Reporting Standards (ESRS) from EFRAG, providing guidance and required metrics.

ESRS 1 and ESRS 2 are mandatory for all CSRD companies, covering strategy overview, risks, policies, and targets, while other standards depend on materiality assessment outcomes.

4. What does a (double) materiality analysis involve?

A materiality analysis involves assessing which sustainability themes are pertinent to your company.

Impact materiality: Evaluates environmental or social themes influenced by the company (inside-out).

Financial materiality: Considers external sustainability-related factors impacting the company's financial status (outside-in).

The European Sustainability Reporting Standards outline criteria for determining materiality. Companies can establish a threshold for a theme to be deemed material or relevant. A theme is material if it's relevant in at least one of the two categories (impact/financial).

Footprint Intelligence offers guidance on conducting a materiality analysis, involving collaboration with your company's working group and stakeholder consultation to address diverse expectations and interests. Our newly created factsheet provides digital and media companies with comprehensive support for conducting their CSRD-compliant materiality assessment.

5. What are the key changes in the final ESRS?

Following public consultation, the European Commission adjusted the draft ESRS standards recently released. Here's a summary of the changes:

Introduction of a phased-in period of 1 or 2 years for specific reporting requirements, primarily for companies with <750 employees.

Increased flexibility in determining which themes are material for each company.

Certain reporting requirements have become voluntary.

1. The extended phase-in period applies mainly to companies with fewer than 750 employees, giving them more time to prepare.

2. Companies now have more flexibility in choosing material themes, potentially reducing costs. However, the 'General disclosures ESRS 2' standard remains mandatory for all companies. Additionally, 'Climate change ESRS E1' is subject to materiality analysis. If a company deems climate change immaterial, it must justify its decision.

3. Some reporting requirements have shifted from 'shall disclose' to 'may disclose,' particularly challenging data points such as the biodiversity transition plan and specific indicators for self-employed and temporary workers."

6. What are the steps to comply with the CSRD?

Achieving CSRD compliance varies for each company, depending on factors like its business nature, phase-in schedule, and existing sustainability reporting status. Here's a summary of suggested next actions:

Define entities required for CSRD reporting, along with any needed accommodations.

Conduct a double materiality assessment to pinpoint relevant ESRS impacts, risks, and opportunities.

Address gaps between ESRS requirements and currently available information.

Collect necessary data.

Prepare for and obtain limited assurance.

7. How to optimize CSRD reporting?

On the journey to CSRD compliance, Footprint Intelligence helps companies streamline the reporting process, leveraging AI to expedite compliance. By harnessing technology, we transform this obligation into a competitive advantage, empowering companies to navigate sustainability reporting with efficiency and precision.